Resource: Hurricane & Flooding Risks in the Southeast

Rising Hazard & Shrinking Insurance Options

Download the PDF of the one-pager, or read the details below:

Background

The southeastern United States is facing the perfect storm of environmental and economic instability. As hurricane and flooding intensity increases, the regional insurance market is fracturing bit by bit, leaving millions of homeowners and renters vulnerable. Traditionally, it is expected that property insurance provides a reliable safety net for coastal recovery; however, the combination of rising sea levels and extreme weather events has shifted the “playing field” for both insurers and residents in the Southeastern region of the United States. Understanding the scale of this crisis is crucial for protecting the economic health of our coastal communities.

Key Takeaways

- Market Exodus & Rising Costs: Since 2022, average premiums in Southeastern coastal zones have surged by 45%, while over 15 major insurers have withdrawn or restricted coverage in the region.

- The “Going Bare” Trend: Approximately 1 in 10 homeowners across the Southeastern states now live without any property insurance.

- Widening Equity Gaps: The crisis disproportionately affects low-income households. There is a 15% uninsured rate for Southeastern households earning less than $50k annually.

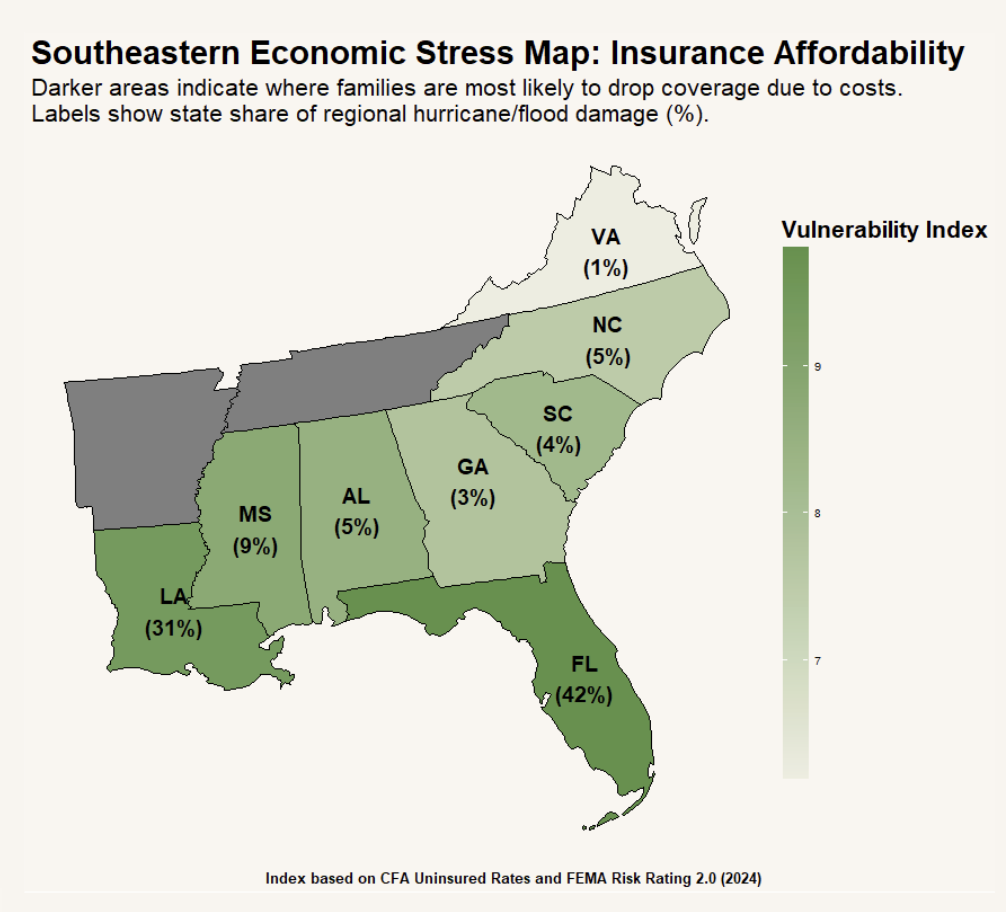

- Regional Vulnerability: Data shows that Florida (42%) and Louisiana (31%) carry the highest share of regional hurricane & flood damage, making them the most “at-risk” zones for total market collapse.

- The Recovery Trap: In 2024, 47% of regional disaster losses were entirely uninsured, creating a cycle of debt and displacement for affected families.

Southern Coastal Crisis: By the Numbers

Compounding regional risks of hurricane damage, market instability, and social inequity.

- Rising Costs: +45% avg. premium increase across Southeastern coastal zones since 2022

- Going Bare: 1 in 10 homeowners across the South now living without any property insurance

- Hurricane Risk: $1.5T total US hurricane damage since 1980 (primarily SE impact)

- Flood Risk: +107% avg. protected flood insurance hike across SE states under Risk Rating 2.0

- Equity Gap: 15% uninsured rate for Southeastern households earning <$50k

- Home Exposure: 32.7M total homes in the SE currently at high risk of hurricane damage

- Market Exodus: 15+ major insurers that have withdrawn or restricted coverage in the SE region

- Disaster Risk: 155% increase in billion-dollar disasters in the SE (past 5 yrs vs avg.)

- Recovery Trap: 47% share of 2024 regional disaster losses that were entirely UNINSURED

Implications for Policy and Practice

- Implement Targeted Affordability Subsidies: Address the equity gap by providing tiered insurance assistance for households earning under $50k.

- Strengthen Market Stability Protections: Develop incentives to retain insurers in high-risk zones and mitigate the “market exodus” seen primarily in Florida and Louisiana.

- Modernize Risk Rating Standards: Utilize updated flood and hurricane insurance projections to help homeowners make informed decisions before they fall into the “recovery trap”.

- Expand Rural & Safety-Net Coverage: Ensure that residents in areas with limited access to private insurers have reliable state-backed alternatives.